If you are running or planning to open a fast-food business – such as takeaway coffee, bubble tea, sandwiches, office lunch sets, or meals under 100,000 VND – there is one customer group you cannot ignore: office workers.

Because the fast-moving consumer (FMCG) model relies on three very clear things: repeated daily purchases, quick decisions, and short travel distances. Office workers go to work 5-6 days a week. They need coffee in the morning, a quick lunch, and a drink in the afternoon. They don't have time to travel far or think too much. They choose what's near, fast, and convenient.

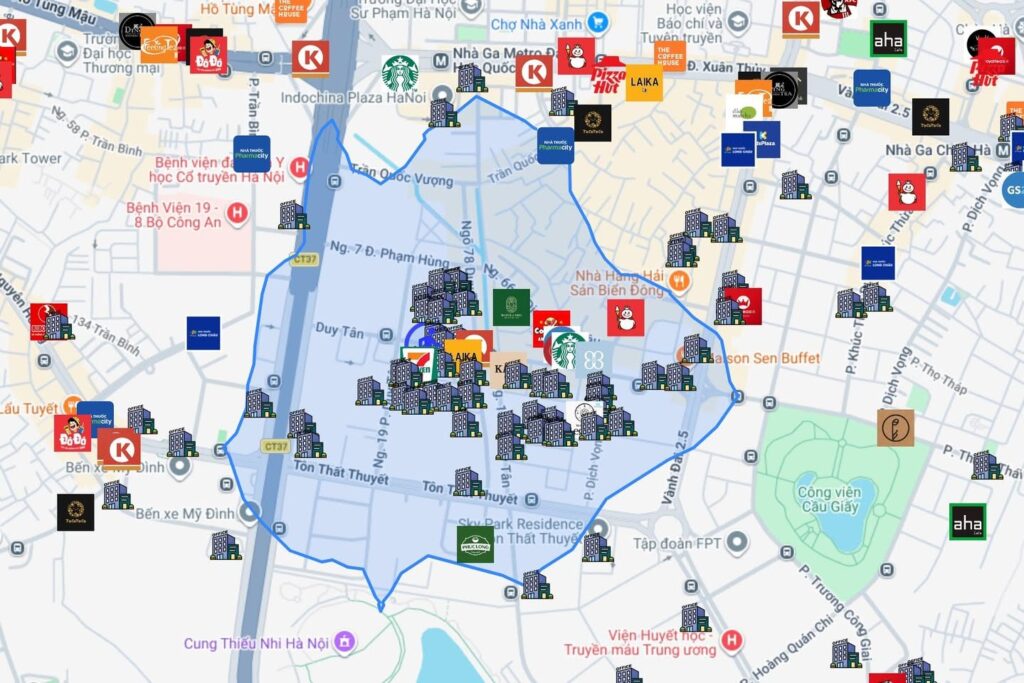

This morning, I opened the map and zoomed in on the Duy Tan – Tran Thai Tong – Ton That Thuyet area. I plotted a 10-minute walking radius around the office core. When I turned on the data layer, the picture became very clear: an area of approximately 75.87 hectares, with a permanent population of just over 8,000 people in about 1,868 buildings. However, the number of office workers operating during the day reaches 75,708 people. This means that during the day, the actual number of people in the area is almost 10 times higher than the resident population. I compiled this figure from data from the General Statistics Office (2019 Population Census and estimates for 2023–2024) combined with data on office buildings and labor force by area.

Looking at the map, it becomes clear: this isn't just an eastern district, but a concentrated consumer cluster. At 11:30 a.m., crowds pour out from dozens of buildings. If your store is within a 300-500m radius in the right direction of traffic, you're practically touching the money flow. If it's off-axis or on the wrong side of the road, you could lose 30-50% of your revenue without understanding why.

According to NielsenIQ, over 60% office workers in major cities eat out at least 3–5 times a week. Euromonitor's Vietnam Foodservice report also shows that the 22–40 age group in urban areas is the main consumer force for the coffee and fast-food segment, with a high priority on convenience and speed. Simply put: they buy frequently and buy nearby.

What I learned from looking at the map wasn't "there are a lot of people here," but "the right people I need are concentrated here." When opening a store, you shouldn't look at the traffic, but at the flow of people going to work. You shouldn't ask "is it crowded?", but "is this the right profile?".

I'm building a map data layer so that anyone opening a store can see this picture: the population density, the number of office workers, their travel routes, and the actual walking radius. Because choosing the right location isn't about luck. It's about understanding the data and understanding customer behavior.

One thing I've realized after many years in this business is that opening a store isn't too difficult, but developing a truly successful store is a completely different story.

Many people think these two things are the same. But in reality, they are very different. Opening a store sometimes only requires finding a location, renovating it, opening for business, and starting to sell. Developing a store, however, is a much longer process, beginning even before the store exists and impacting it for many years afterward.

Having worked in this field for a long time, I've realized that developing a store is actually a very comprehensive job. It's not just about finding a location. Those in this profession have to go through many things that outsiders often don't see. There are times when you just stand on the street observing the flow of traffic and people, watching where they stop, how they pull over, or if they just drive by and go on. There are times when you have to sit for hours in a coffee shop to get a feel for the "true flow" of that area.

But observation is only a small part of it. Then there's a whole series of other questions: who are the customers in this area, is it right for the business model I intend to open, what is the purchasing power of that area, and how much revenue would I need to generate to cover the costs if I rent this location? Sometimes I have to sit down and break down each number to see if the calculation is reasonable.

Next comes the contract. Developers must carefully read the lease agreement: clauses regarding price increases, lease duration, repair rights, termination rights, etc., because even a small detail can cost the business dearly later on.

But the work doesn't stop there. There are points to inquire about regarding land and property law, zoning regulations, business licenses, and fire safety. Sometimes you have to work with the landlord, the real estate agent, and the neighbors. There are even cases where you have to go to the local ward or ask the local police to ensure that there won't be any problems when you open the store later.

Jokingly speaking, the job of developing a retail store is like a combination of all sorts of things: market research and analysis, negotiation, contracts, legal matters, working with local authorities… you have to know a little bit about everything, and sometimes you even have to handle things yourself.

The more I work, the more I realize an important thing: the risks of a business location often lie not in the present but in the future. Before opening, everything seems fine. Busy street, beautiful storefront, new building, and the rent seems reasonable. But when you look closer, you see many problems that nobody initially noticed. There are places with lots of traffic but not the target customers. There are places that look bustling but customers only pass by instead of stopping. There are places that look very promising but after only a few months of opening, the revenue isn't enough to cover the costs.

I've met many passionate shop owners. Their products aren't bad, the space is well-invested, and they put in a lot of effort to run it. But in the end, they still struggle to keep it going. Not because they did something fundamentally wrong, but because from the start, the shop was placed in a location that wasn't really suitable. When the foundation is wrong, the more you try to run it, the more tiring it becomes.

Therefore, I've always thought that the store development profession is actually about helping businesses reduce the probability of making the wrong choice. A location decision isn't just about whether or not you can open a store, but about the store's cash flow for many years to come. Rent, initial investment, staff, operations… it all starts with one choice: where to open.

Interestingly, this profession is also somewhat "lonely." When things go well, few remember what the person who chose the location did. But when things go wrong, the question often comes back immediately: "Why did you choose this location back then?" Perhaps that's why a good developer isn't someone who visits the most locations, but rather someone who can spot risks others don't see and dare to say no to seemingly perfect locations.

After many years in the business, I've realized that most store failures don't start with marketing or operations. They begin much earlier, from the moment the business decides where to open.

Simply saying "it's crowded," "it has a nice storefront," or "it looks okay" is usually not enough. Opening a store can be quick, but developing a truly successful business requires a lot of thought before signing the contract.

These past few days, retailers have been talking a lot about Coolmate, a fashion brand that rose to prominence online, opening offline stores. For many, this is quite surprising, as Coolmate was once considered a very typical D2C case: selling online, optimizing its supply chain, and employing strong digital marketing. But if you look at the broader context of the current retail landscape, this move is actually quite logical.

About three years ago, while talking to some retail business owners, I shared a rather simple idea: sooner or later, big online brands will have to open offline stores. At the time, many didn't believe me; some even said bluntly, "You're just focusing on physical stores, so you only value offline ones. They're making hundreds of billions selling online!" I just laughed and said, "Really?" Actually, that idea came from a book I read quite a while ago, "The Unique Retail Experience" by Steven Dennis. This book clearly states that retail isn't dead, it's just changing shape. And one of the biggest changes is that customers no longer buy based on channels, but based on experiences.

Looking at the Vietnamese market in recent years, the picture is very clear. E-commerce is growing extremely rapidly. In 2024, the size of the Vietnamese e-commerce market exceeded $25 billion and continues to grow strongly every year. In 2024 alone, Vietnamese people spent approximately $16 billion on online shopping, equivalent to more than $40 million per day. However, if we put this figure into the total retail market, e-commerce still only accounts for about 8-10% of total retail sales in Vietnam. This means that online sales are growing very quickly, but offline sales still constitute the majority of the market.

But the biggest problem with online selling today isn't the market size, but the ever-increasing costs. In the early years of the e-commerce boom, many platforms strongly supported sellers: low fees, subsidized shipping, and lots of free traffic. But in recent years, the story has started to change. Shopee has adjusted its fees from around 41 TP3T to 101 TP3T depending on the product category, while TikTok Shop and other platforms have also continuously increased commission and transaction fees. If you add payment fees, promotional programs, free shipping, affiliate fees, etc., the total cost of selling on these platforms can now range from 9–151 TP3T of revenue, and in some cases even up to 171 TP3T.

To put it simply, if you sell a product for 500,000 VND on an e-commerce platform, the platform fees and operating costs alone could amount to around 60,000–80,000 VND. This doesn't even include advertising costs, livestreaming, KOLs, affiliate marketing, etc. Many brands are actually spending 20–30% of their revenue on online marketing just to maintain sales momentum.

Let's take a simple example to make the comparison easier to understand. Suppose a brand sells shirts at an average price of 350,000 VND. If they sell on e-commerce platforms, the platform fees and promotions are around 121 million VND, meaning each order costs about 42,000 VND. If they sell 10,000 orders per month, the platform fees alone would be around 420 million VND. This doesn't even include advertising. Meanwhile, if an offline store in a central location costs around 120-150 million VND/month in rent, plus operating costs, it could reach around 200 million VND. But that store, besides selling directly, also helps increase brand awareness, increase online purchases, reduce advertising costs, and create a better customer experience. In other words, the cost isn't just the cost of selling, but also the cost of marketing.

Therefore, many online brands are beginning to view offline stores from a different perspective: not just as points of sale, but as a marketing and experiential channel. This is also something Steven Dennis emphasizes frequently in his book: today's stores are more like a "media channel" than just a place to sell goods. They help customers try products, understand the brand, create content, and build trust. And in a world where online advertising is increasingly expensive, these physical touchpoints become crucial.

From a real estate perspective, I also see a rather interesting signal. When zooming in on the Mapdy app in the central area of Ho Chi Minh City, within a 500m radius, I found more than 140 street-front properties listed for rent. This indicates a fairly large supply of commercial space after a period of market volatility, but at the same time, demand from brands is returning. In fact, recently I've seen many brands starting to re-evaluate locations, especially those with a strong online presence.

Ultimately, it's not about whether online wins over offline or offline wins over online. Each business will have a different strategy. Some brands are suited to online, some need a strong brick-and-mortar store system, and many choose a hybrid model. The most important thing isn't choosing which channel, but understanding your customers and designing an experience that suits them.

The retail world is changing rapidly. What worked yesterday may not work tomorrow. And perhaps that's why brands like Coolmate are starting to move away from online to experiment with new channels. It's not because online is no longer good, but because retail today is a story of a multi-channel ecosystem – where online and offline support each other.

A few days ago, I went to view a location in the Bac Hai area to open another branch for an art center I'm advising. The location was nice, the structure was good, and the rent was reasonable. Honestly, if I followed my "market intuition," I could almost close the deal, with only a few minor clauses left to sign. But right then, the Founder asked me a very short question: "Will this affect sales at the Tan Binh store?" I paused, because conventional thinking is that these two areas are separated by the Nhieu Loc canal, so we often assume it won't have much impact. But my experience running a chain of stores has taught me one thing: geographical intuition is often wrong; customer movement is what ultimately matters.

I opened Mapdy, plotted the motorcycle travel zones within a 5-10 minute radius as shown in the image, and the results were clear: these two zones overlap strongly, meaning the same customer base can visit both stores within the same timeframe. Simply put, this isn't about opening more locations to attract more customers, but rather about redistributing existing customers. In retail, this is called cannibalization, and according to industry data, if two stores are within a 10-minute travel radius, the "sales cannibalization" rate can reach 20-70% depending on the industry and consumer behavior.

Let me give you a very practical example to help you visualize: store A is making 600 million VND/month, then opens store B. After that, A has 400 million VND left, and B makes 200 million VND. At first glance, it seems like there's an additional 200 million VND in revenue, but in reality, the total remains 600 million VND, not an increase. Meanwhile, rent, staffing, and operating costs all increase, meaning profit decreases. This is a trap that many store owners fall into but don't realize, because they think opening the new store is the right decision since it's still generating revenue, without looking at the overall system.

The biggest mistake here is that many people only look at the attractive location, good price, and high foot traffic without answering the most important question: are these customers new or existing customers? Without data on traffic patterns and a view of catchment areas like in the image, it's almost impossible to answer accurately. In reality, many "barriers" like canals, main roads, or perceived distances become less significant when motorbike travel within the city is so flexible.

Ultimately, the team decided against renting the space in Bac Hai, not because it wasn't good, but because opening a new store wouldn't create additional value. The insight was simple, yet many overlooked it: opening more stores isn't about having more stores, but about having more customers. Without more customers, you're just repackaging the old pie. And sometimes, the decision not to open… is the decision that will help you make the most money.

The Vietnamese retail market is growing, but not everyone who opens a new store will succeed. This is something I thought about a lot while reading Q&Me's Modern Trade 2026 report.

On the surface, the picture looks quite good. Total retail sales of goods and consumer service revenue in 2025 are estimated at VND 7,008,932 billion, an increase of 91% compared to the previous year. Retail sales of goods alone reached VND 5,335,113 billion, an increase of 81%, while food and accommodation increased by 13% and tourism by as much as 33%. In other words, purchasing power remains, consumer spending continues to flow, and Vietnam remains an attractive enough market for many chains to continue expanding.

But upon closer reading, I discovered a very thought-provoking truth: a rising market doesn't necessarily mean every location is good, and a booming industry doesn't necessarily mean every brand that opens a new branch is the right choice.

Because when the number of stores increases too rapidly, the question is no longer "should we open one?", but "where should we open one so we don't self-destruct?".

Looking at this report, five things are very clear.

Firstly, the strongest wave of expansion is not in large-scale models, but in models with dense, convenient networks and high purchase frequency. The mini-supermarket/convenience store/pharmacy group is a clear example. The total number of convenience stores/mini-supermarkets in the report is projected to reach 9,703 locations by 2026. WinMart+ alone increased from 3,692 to 4,592 stores in one year, an increase of 900 locations. Bach Hoa Xanh increased from 1,864 to 2,759, an increase of 895 locations. Kingfood Mart increased from 96 to 141. In the pharmacy group, the entire chain market is projected to reach 4,088 stores by 2026; Long Chau alone reached 2,381 locations, Pharmacity 1,065, and An Khang 415.

This shows that what's winning isn't just strong brands, but models that can be quickly replicated in "sufficiently usable" locations, near residential areas, and with high repeat customer traffic. This is a huge change. In the past, many people thought that opening a chain required waiting for a "prime corner," a "beautiful intersection," or a "prestigious storefront." But current data shows that many fast-growing industries thrive on their ability to spread evenly across residential areas, rather than just a few show-off locations.

To put it bluntly: with frequent purchases like food, medicine, and convenience items, the question is no longer "is this house nice?", but "is this house located within the convenient radius of the neighborhood?".

Secondly, growth is strongly shifting away from Ho Chi Minh City and Hanoi. The report reiterates this across many sectors. The fast food sector, as noted by Q&Me, has seen significant growth, particularly outside of Ho Chi Minh City and Hanoi. KFC increased from 172 to 240 stores, Lotteria from 222 to 262, McDonald's from 37 to 47, and the total fast food sector is expected to reach 1,156 stores by 2026, with "Others" accounting for 629 locations, significantly higher than Ho Chi Minh City's 338 and Hanoi's 189. For pharmacies, the "Others" sector reached 2,496 stores out of a total of 4,088. Similarly, for coffee chains, the "Others" sector also reached 2,508 stores out of a total of 5,159.

I really like this detail because it highlights something many people opening new stores often miss: growth opportunities are no longer solely limited to the two major cities. Ho Chi Minh City and Hanoi are still the places to establish brand identity, test formats, and build awareness. But to scale, to increase the number of locations, to achieve more reasonable rental costs, and to broaden market coverage, chains are aggressively expanding into second- and third-tier provinces and cities, as well as satellite urban areas.

This leads to a completely different problem regarding location. In the centers of Ho Chi Minh City or Hanoi, people often compete for a property because of its visibility. In the provinces, however, the challenge is usually finding a property on a main thoroughfare – in the right place with high foot traffic – in the right cluster of needs – and within the right rental price range. Anyone who applies the mindset of "a prime location in a major city center" to the provinces is likely to make a mistake. In the provinces, a successful store isn't often located on the most prestigious street, but rather in a convenient location near home, easy access to transportation, close to markets, hospitals, schools, and new residential areas.

Thirdly, the market is not growing uniformly; some sectors are expanding rapidly, while others are contracting significantly. This is the part that business people should read very carefully.

The sectors experiencing strong growth include coffee chains, fast food, kids/baby stores, drugstores, and mini-supermarkets. Coffee chains are projected to increase to 5,159 stores in 2026; Highlands to 928, Phuc Long to 249, Starbucks to 149, Katinat to 120, while The Coffee House will decrease to 82. The kids/baby sector will reach 1,449 stores, led by Con Cung with 1,037, Kids Plaza with 192, and AVAKids with 91. Drugstores, as mentioned, are experiencing strong growth. Fast food is showing significant increase, especially KFC and Lotteria.

Conversely, mini-stores decreased to 100; fashion stores fell from 1,442 to 1,263; and BBQ/hotpot/others stores also declined from 621 to 602. Traditional milk tea chains weakened, with reports indicating a decline in well-known chains and a rapid rise in the affordable milk tea segment. Bakeries/sweets stores generally remained flat or saw a slight decrease in major cities.

So how should I read it?

In my opinion, this isn't just a matter of "hot industries" or "outdated industries." More profoundly, it reflects the degree of suitability between the business model and current rental costs, as well as the frequency of consumer behavior.

Models with high purchase frequency, quick decision-making, convenient location, easy replication, and moderate size will handle leasing challenges better. However, models that rely on long-term customer experiences, high ticket sales, large space, complex operations, or must be in prime locations to survive will see profits evaporate quickly if just one or two parameters are chosen incorrectly.

In other words, at this stage, premises are no longer simply a fixed cost. They are a strategic filter of the model.

Fourth, many chains are increasing in number, but the rate of increase is no longer the sole objective; the quality of the network is becoming more important. Just look at the case of The Coffee House, which decreased from 141 to 93 and then to 82. Or in cosmetics, The Body Shop and The Face Shop continue to shrink. In fashion, many chains are maintaining or decreasing. Conversely, chains that are growing well are usually those that have found a clearer replication formula: Hasaki, Long Chau, WinMart+, Bach Hoa Xanh, Highlands, KFC…

This is what I want to emphasize to those of you who are preparing to open a new store: opening more stores is not a sign of success. Sometimes it's just a sign that you're spending your capital faster.

The important question isn't "how many points are the opponent scoring?", but rather:

What business model are they using?

What are their standard floor plans?

Which buying behavior are they targeting?

And is the unit economics of each point truly sustainable?

If you can't answer those four questions, it's easy to get caught up in the illusion of growth.

Fifth, and perhaps the most important thing for those looking to rent: read industry data to understand what type of space you should be looking for, not just to find an excuse to open a business anywhere.

For example, if you're running a chain coffee shop or a quick-service F&B business, reports show the industry is still growing, but competition is intense. This means simply having a "nice" location isn't enough. You need to consider accessibility, parking, traffic flow, population radius, office clusters, schools, and customer habits. A market with 5,159 chain coffee shops doesn't reward latecomers based on sentiment. It only rewards those who truly understand the micro-level needs of each location cluster.

If you're running a convenience store, pharmacy, or mother and baby shop, this data suggests that opportunities lie in residential areas and suburban regions. In that case, the criteria for location must change: it doesn't necessarily need to be a "prestigious" location, but rather one situated in a well-connected area, with convenient access, reasonable rent, and the potential for mass replication.

If you're in fashion or a long-term experiential business model, data is warning that opening a store now can't be done with a simple "just grab a nice store" approach. This sector is under immense pressure regarding store performance. Each store must play a clear role: a flagship for brand building, a satellite store for closing deals, or a showroom to support online sales. Unclear roles can easily lead to silent losses.

From this report, I've drawn four very practical lessons for those who are opening a branch.

First, don't look at industry growth and assume your market will win. Industry growth is macroeconomic data. Market performance is a microeconomic issue. Between those two things lies a whole layer of analysis about customers, service radius, competitors, rental levels, accessibility, and traffic flow.

Secondly, the more competitive the market, the less you can choose a location based on intuition. This is especially true for coffee shops, fast food restaurants, convenience stores, and pharmacies. Large chains don't build on trust. They build based on criteria, financial models, humane standards, and a disciplined approach to eliminating flaws.

Thirdly, the era of chains that know how to "cover the right area" is coming, not just "opening many stores." Looking at WinMart+, Bach Hoa Xanh, and Long Chau, this is very clear. The challenge is to cover the right clusters of needs, the right lifestyles, and the right behavioral radius.

Fourth, a good location today must answer the business question: who does it serve, where does it attract customers from, how does it generate revenue, can it be expanded to nearby locations, will it affect internal sales, and can the rent be sustained for 24–36 months?.

If you ask me what the biggest mistake people make when opening a real estate agency right now is, I would say: reading about market growth and then going to look for properties, instead of understanding your business model first and then looking for the right type of property.

The Vietnamese market is still offering many opportunities. This report clearly demonstrates that. But opportunities now don't reward the quickest movers. They reward those who read the right data, understand the market correctly, and choose the right platform.

Having developed convenience stores for over 12 years, I've come to realize one thing more and more clearly: with the convenience store model, the question isn't "is this location good?", but rather "is this location aligned with the customers' daily routines?". And if you look at how these chains are operating, especially when scrutinizing the map, you'll see a very clear pattern: convenience stores are closely clustered around apartment complexes and office buildings.

This is not a coincidence. This is a strategy.

Let's look at the market picture first. According to Q&Me data I read, the convenience store/mini-supermarket group alone will reach approximately 9,703 stores nationwide by 2026. Within this, mini-supermarket chains are experiencing strong growth, especially WinMart+ with 4,592 stores and Bach Hoa Xanh with 2,759 stores. As for the truly convenient store group, close to the quick-purchase, quick-visit, high-frequency model, Circle K has 500 stores, GS25 has 318, Mini Stop 184, Family Mart 172, and 7-Eleven 148. Circle K and GS25 alone have 818 stores, notably concentrated in the two major cities: Circle K has 223 stores in Ho Chi Minh City and 191 in Hanoi; GS25 has 196 in Ho Chi Minh City and 46 in Hanoi.

This number reveals two very important things.

Firstly, this market is no longer in its experimental phase. It's a game big enough that chains understand very well what they need to stick to in order to survive.

Secondly, the strong concentration in Hanoi and Ho Chi Minh City shows that the convenience store model is heavily dependent on urban density, a fast-paced lifestyle, accessibility via walking or quick visits, and especially the demand for repeat business throughout the day. And where does that demand come from? In apartment buildings and office buildings.

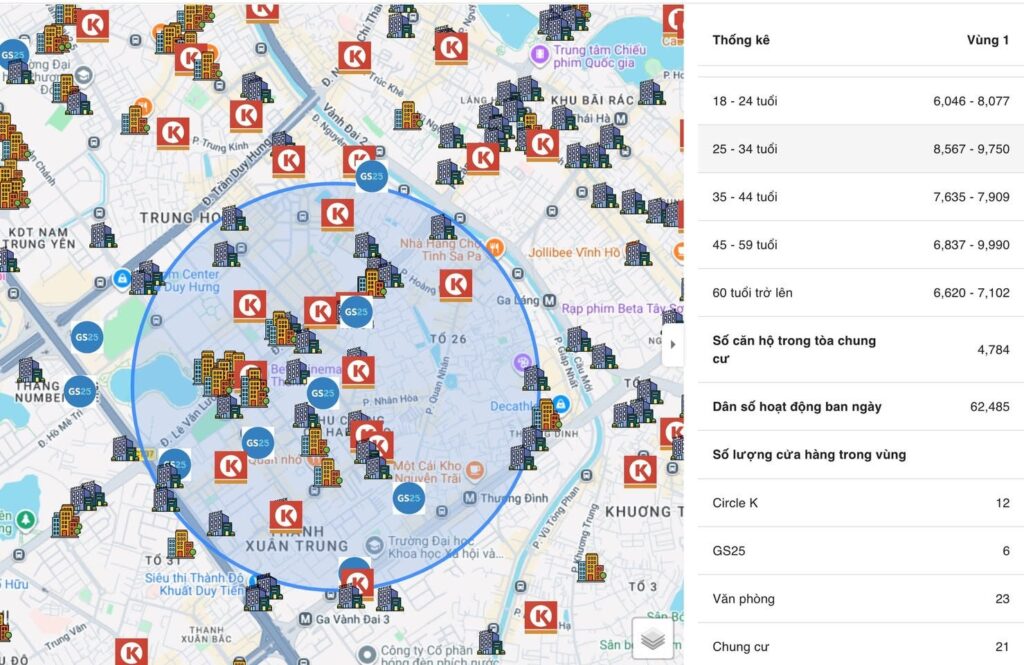

When I looked at the map, the first thing that caught my eye wasn't the number of Circle K or GS25 logos. More importantly, it was how they were strategically placed in areas with high building density, dense residential clusters, and distinct office cores. In the area circled on Mapdy, within the same market zone, there were 12 Circle K stores, 6 GS25 stores, along with 23 office buildings and 21 apartment complexes. Additionally, this area had 4,784 apartment units and 62,485 people with a daytime working population.

This data is very expensive.

Because if you only look at the surface, many people will simply say, "This area is crowded, so there are many businesses." But those in the business won't stop at just "crowded." We need to clearly differentiate: who is crowded, when is it crowded, why is it crowded, and what activities are generating the revenue?.

For convenience stores, the key to survival isn't pure traffic, but rather repeat purchases and convenience on the go. Customers of this model don't always make large, planned purchases like they do at supermarkets. They have very short-term, everyday needs: buying water, coffee, snacks, late-night meals, personal items, paying utility bills, waiting, sheltering from the rain, using the air conditioning, or quickly buying something they forgot to prepare. In other words, a convenience store's revenue comes from many "small transactions," but in return, it requires something extremely large: a continuous, recurring demand around the point of sale.

Apartment buildings create that "repetition" during early mornings, evenings, weekends, and short breaks throughout the day. Office buildings create that "repetition" during rush hour, lunch breaks, afternoons, after-work hours, and even urgent purchases throughout the day. In other words, apartment buildings give convenience stores a resident customer base, while offices give them a daytime customer base. When these two classes overlap, the store essentially generates revenue across multiple time slots, rather than relying on a single peak in sales.

That's why I always say: for convenience stores, a good location isn't just about being "busy," but about having two overlapping rhythms of life. During the day, there are offices generating revenue. In the evening, there are residents generating revenue. And on weekends, there's still the support of the local community. That model is much safer than a location that's only appealing to one group of customers.

Now let's go back to the Mapdy numbers in the circled area. 4,784 apartments represents a very significant population. If we convert that to the number of households, the daily demand for small purchases would be enormous. Not all residents shop at convenience stores, but even a small percentage with a habit of frequenting them would be enough to generate a stable revenue stream. Meanwhile, the 62,485 daytime active residents indicate that this area is not just a place to live, but also a place for work, commuting, and daytime consumption. This is a crucial indicator, as it helps us understand that this area doesn't "sleep" during the day. It has real commercial vitality.

Next, let's look at the competitive structure: in the same area, there are 12 Circle K stores and 6 GS25 stores. Many people might think this indicates saturation. But if you understand the logic of the industry, that's not necessarily true. A large number of stores doesn't automatically mean overcrowding. It usually reflects one thing first: the market is good enough for many chains to operate there. In other words, if an area isn't generating revenue, there wouldn't be so many experienced chains vying for it.

Of course, at some point there will be internal sales competition and pressure. But in the CVS model, the distance between stores is usually much shorter than in other industries, because the nature of the game is about securing the nearest touchpoint. Convenience stores sell "convenience," and when selling convenience, a distance of 200-500 meters can sometimes make a difference. Customers aren't always loyal to a brand based on its products. Often, they are loyal to the store closest to their route, easiest to access, the first to see, and the quickest to enter. Therefore, the chain's strong presence in apartment buildings and offices is not only to attract customers, but also to block competitors, capture customer habits, and secure consumption areas before others enter.

That's why I say the strategy of targeting apartment buildings and offices for convenience stores is a very logical one, very difficult to refute if you look at the true nature of the industry.

Firstly, apartment buildings offer a much higher density of households on a small plot of land compared to sprawling townhouses. An apartment building brings together hundreds, even thousands, of apartments in one location. This means that within a short walking radius, the store has access to a huge customer base. This is exactly what convenience stores need: not a large market, but a compressed market.

Secondly, office buildings generate purposeful traffic, quite different from casual, sightseeing traffic. Office workers consume in a very clear rhythm: morning coffee, snacks, drinks, lunch breaks, personal items, afternoon snacks, and quick purchases after work. They don't need many reasons to buy, just convenience and speed. This type of need is perfectly suited to convenience stores.

Third, by targeting both these layers, the store reduces the risk of dead time slots. A location relying solely on offices is easily susceptible to losses on weekends or evenings. A location relying solely on residents might be weak during business hours. But with both residents and offices, the daily revenue curve is usually thicker, more attractive, and more sustainable.

Fourth, this model also helps the chain optimize logistics and brand recognition. When many locations are clustered in similar urban areas, the chain can easily standardize location selection criteria, expand within the cluster, manage deliveries, and create a sense of "being present everywhere." In the convenience industry, a dense brand presence is a key part of competitive advantage.

But let's be frank: simply being near apartment buildings or offices doesn't guarantee success. This is a common misunderstanding among those outside the industry.

The biggest mistake is viewing apartment buildings as a homogeneous sphere. Not all apartment complexes cater to the same needs. High-end apartments, mid-range apartments, older apartments, areas with strong shophouses, areas with residents who rarely walk to the ground floor, or areas with mini-supermarkets within the complex… each type caters to different consumer behaviors. Some areas have a large population but they shop at large supermarkets weekly, rarely visiting CVS. Other areas have young, single residents who live fast and make small, individual purchases. And in some areas with many apartments, the purchasing power at convenience stores is low due to inconvenient access, difficult parking, or stores being hidden from view on the way home.

The second mistake is viewing office space as merely an added bonus for aesthetics. In reality, having many buildings isn't necessarily a good thing. You need to consider the type of office, its size, occupancy rate, workforce composition, operating hours, whether there's strong competition from food and beverage establishments, and most importantly: the direction of traffic flow from the building. An office across the street that's inconvenient for clients to cross is almost meaningless.

The third mistake is looking at the number of competitors without understanding the context. In some areas, 5 stores are already too crowded. In others, 15 stores still offer opportunities. The issue isn't the absolute number, but rather the overall demand, the distribution structure, and the degree of fragmentation of the customer base. With Mapdy, the key is not just counting competitors, but also understanding which demand segments they're targeting and which areas are truly "breeding ground" for the model.

I want to emphasize another point that store developers must be extremely vigilant about: convenience stores aren't simply about being located in apartment buildings and offices, but about being situated at the intersection of residential areas, workplaces, and transportation routes. Apartment buildings and offices are just two major magnets. To choose the right location, you still need to consider factors like the storefront's visibility, accessibility, parking availability, quick entry points, visibility of the signage, whether the storefront catches pedestrian traffic, and whether evening commuters pass by the storefront. In other words, data helps in choosing the right area. Success, however, depends on selecting the right landing spot within that area.

From a chain strategy perspective, I believe what convenience store chains are doing is more than just "opening stores in densely populated areas." They are building a network that covers the fastest-paced urban areas. They target apartment buildings to retain resident customers, offices to capture daytime consumer traffic, and clusters to increase presence density. And they place stores in locations where customers are likely to visit almost without much thought.

That's why I don't view convenience stores as simply a retail model. They are a model that seizes the power of convenience in urban life.

And if you reread the data you sent, everything fits together perfectly. Q&Me shows that the market is already large enough, competitive enough, and the major chains are still firmly entrenched in the two major cities. Mapdy shows that in a typical market area, there's already a structure that convenience stores love: 4,784 apartments, 62,485 daytime active residents, 23 office buildings, 21 apartment complexes, along with a strong presence of Circle K and GS25. This isn't a random picture. This is a picture of a store expansion strategy based on very clear demand logic.

To sum it up briefly: convenience stores win not because they sell the cheapest products, nor because every location they enter is prime. They win because they understand a fundamental principle of urban retail: to generate repeat sales, they must be located where people repeat their lives. And in large cities, this is most evident in apartment buildings and office buildings. And they are drawn to convenience, as the name suggests.

While working, my older brother sent me a video analyzing the situation of businesses returning premises on Ho Van Hue Street. After listening to it, it seemed reasonable. Actually, the story of shops withdrawing from this street has been going on for 3-4 years now, not just recently. But every time a few streets become vacant, there's a wave of conclusions that the market is tough and businesses are returning en masse. While that sounds reasonable, it doesn't accurately reflect the current situation.

Looking back over a decade, when online shopping wasn't as developed and customers still searched for physical stores, the "specialized street" model worked very well. Fashion was concentrated on Nguyen Trai and Le Van Sy streets; F&B on Phan Xich Long; wedding dresses on Ho Van Hue street… But now, behavior has changed. Customers search on their phones first before deciding where to go. Streets like Ho Van Hue face another major problem: inconvenient access, difficulty parking, and not being on the main traffic flow. Therefore, the withdrawal of brands was predictable. Bringing up this issue again to say the market is struggling is inappropriate in the current context.

However, looking at the current reality, the story is completely the opposite. Finding a good location is not easy these days; in fact, it's scarce. Even I and my colleagues in the business are struggling to find a place to open a store. Having money doesn't guarantee a spot. There are clear examples: yesterday the landlord was asking 70 million VND, the next day they've raised it to 80 million VND, and people are still inquiring about renting. This is no longer an isolated incident but a sign of a price increase cycle returning.

Why is that? Actually, there are three forces pushing the market up simultaneously.

Firstly, there's a wave of brands that previously sold online returning to offline. After a period of dependence on e-commerce platforms, with increasingly high costs, many realized that platform fees and advertising could account for 20-30% of their revenue, so they started opening physical stores to optimize their profits.

Secondly, large chains continue to expand very aggressively. The convenience store and mini-mart sector alone in Vietnam has nearly 10,000 locations, with WinMart+ having over 4,500 stores, not to mention F&B chains like Highlands, Phuc Long, Katinat… which open dozens to hundreds of new locations each year. Wherever these brands expand, the price of retail space in that area is driven up.

Thirdly, there's a wave of international brands returning to Vietnam after the pandemic. They're not going individually but in groups, following long-term strategies and willing to pay high prices to secure their positions. For example, a Chinese bubble tea chain recently entered the market with positions costing hundreds of millions of VND per month. And while the press recently reported that the king of burgers closed all his stores, another major player is now reportedly entering Vietnam.

The most dangerous aspect is that the game has changed, something many people haven't realized. In the past, if you opened an art school, you only competed with other art schools; if you opened a gym, you competed with other gyms. Now, you're competing for space with large F&B chains, high-net-worth online brands, and even international brands. The game is no longer about competing within the same industry, but about who can afford the higher costs and for the longer term. And in this game, the biggest beneficiary isn't the business owner, but the landlord.

There's a very real thing about the Vietnamese market: land prices may stagnate for a while, but they almost never fall. When the market slows down, you see many vacant spaces, but when money flows back in, prices rebound very quickly. So, if you look at the true nature of things, the market isn't dying, but rather undergoing a phase transition, and the frenzy of rising land prices is about to return.

For those preparing to open a business right now, the crucial question is no longer "how much will the rent cost," but whether their business model can handle these costs. Most mistakes don't lie in the search for a location, but in realizing after signing the contract that they're entering a much bigger game than they initially imagined.

I just read an article about "40,000 Chinese convenience stores preparing to enter Vietnam," and to be honest, my feeling isn't one of worry, but rather... a sense of familiarity. This market has seen too many "big waves" of entry already, and most stories don't end as initially expected. Hearing about 40,000 stores sounds impressive, but it's important to understand: that's the scale in China; in Vietnam, they're currently only testing it out in a few locations. And in this industry, having a large-scale model abroad and achieving success in Vietnam are two completely different stories.

Looking back at history, we have no shortage of cases to learn from. Take Shop&Go, for example, which had nearly 90 stores after more than 10 years of operation, but ultimately sold the entire system for just $1. Or Auchan, a large French retail group, which entered Vietnam with a well-planned strategy and invested tens of millions of dollars, but after only a few years had to withdraw and transfer its entire system. More recently, the press reported that Burger King closed all its stores, and people in the industry mentioned that many of their Chinese snack chains are also closing… These are businesses that didn't lack money or experience, yet still failed. The reason wasn't about scale, but about not understanding the market deeply enough and, especially, making mistakes in choosing locations, driving up rents to expand.

In Vietnam, the most difficult challenge isn't operations or marketing, but finding suitable locations. In reality, prime locations have been largely secured by large chains like Circle K, GS25, 7-Eleven, WinMart+, and Bach Hoa Xanh. According to recent data, WinMart+ alone has over 4,500 stores, Bach Hoa Xanh nearly 2,700, and the entire convenience store and mini-mart market is close to 10,000 outlets. This means that the "prime land" in the market has already been largely divided, and newcomers almost certainly have to accept one of three things: higher rent, less desirable locations, or a significant amount of time spent rebuilding their network.

And when another major player enters the market, it's certain that rental prices will continue to be pushed up. I've personally observed this on many streets in Ho Chi Minh City; with just 2-3 competing chains on the same street, rental prices can increase by 20-50% within 1-2 years. Meanwhile, the convenience store model has a relatively low profit margin, typically fluctuating around 20-30% at the gross margin level, but after deducting costs for rent, personnel, utilities, 24/7 operation, etc., the actual net profit is very thin. This leads to a paradox: the faster you open a store but choose the wrong location, the faster you lose money.

One mistake I see repeated many times is "scaling too early." When a business model gets off to a good start, many businesses tend to expand rapidly to gain market share. But without a clear store expansion plan, control over radius and customer overlap, stores will start cannibalizing each other. This is why many chains look like they have many stores on the outside, but their cash flow is very strained internally. And when the cash flow can't handle it, the "filtering" phase begins: closing stores, cutting losses, or even withdrawing from the market.

The Vietnamese market follows a very clear pattern: there's always a cycle of hype to attract attention → rapid opening → filtering → closure. The previous wave of 19,000 VND fixed-price stores is a prime example; they opened very quickly and spread widely, but then almost all disappeared due to inability to withstand the pressure of costs and rent. The story of convenience stores is no exception to this rule, only on a larger scale and possibly faster.

Personally, I don't think the entry of a Chinese chain is a negative thing. On the contrary, it will make the market more competitive and professional. But precisely because of that, it will make the playing field much tougher. Higher rents, higher operating standards, and more costly mistakes. In that context, it's not about who has more money, but who understands the market better, chooses the right location, and has better long-term prospects.

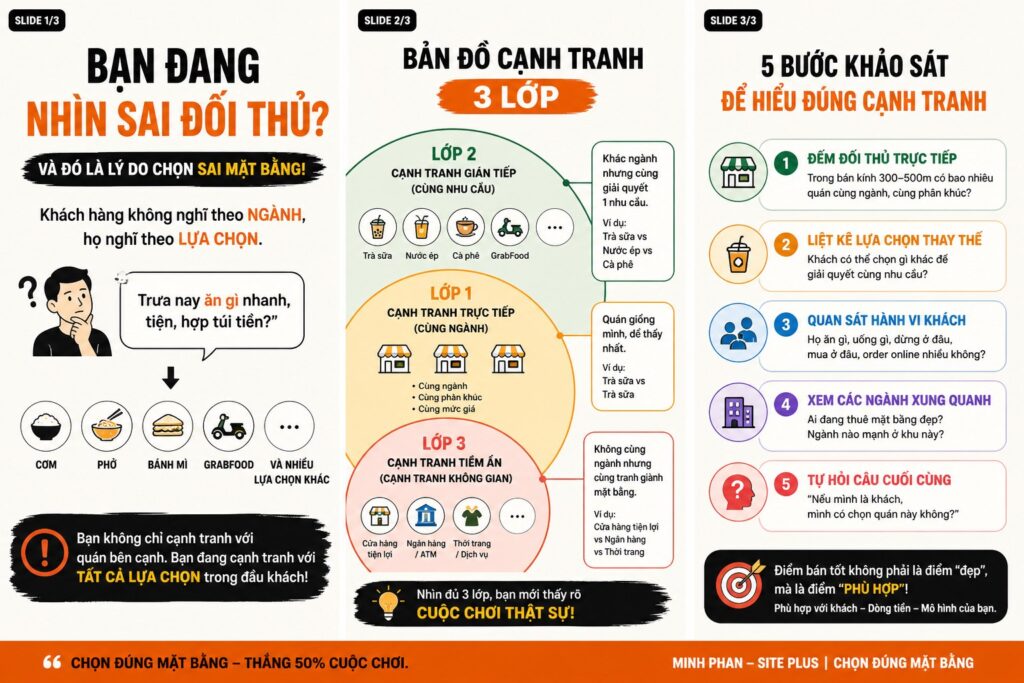

I've done a lot of surveys with clients, and almost eight out of ten people start with the same question: "How many similar restaurants are there around here?" This isn't wrong, but it's too incomplete. And if you only rely on that to make a decision, you're essentially betting your money on an incomplete picture.

The problem lies in the fact that we view competition within a specific industry, while customers make decisions based on "options at that moment." According to several F&B market reports in Vietnam (iPOS 2025), an urban consumer may have 5–10 different food/drink options within a radius of 1–1.5km (≈ 5 minutes by motorbike). This means that when you open a restaurant, you're not just competing with 2–3 similar establishments, but are actually competing within a much larger "menu of choices." And consumer behavior data also shows that over 60% (over 3000 consumers) make impulsive decisions about food and drink, without prior planning; in other words, whoever offers the "more convenience" wins.

Therefore, if you only count direct competitors, you're missing out on a large part of the game.

In practice, I always view competition from three perspectives, and each perspective has data to verify, not just subjective feelings.

Level 1 is direct competition – within the same industry and segment. This is the most obvious: bubble tea vs. bubble tea, coffee vs. coffee. You can quickly measure this with a few metrics: the number of stores within a 300-500m radius, average price (for example, popular bubble tea is 30k-60k VND), and customer volume during peak hours (count the flow in 15-30 minutes). An area with more than 5-7 shops in the same segment within a 300m radius is almost saturated in terms of brand recognition. But the paradox is: this most obvious competition doesn't determine success or failure, because they all look the same.

Layer 2 is indirect competition – same demand, different industry. This is a layer that most people overlook, but it directly impacts revenue. A very specific example: according to data from food delivery platforms, in Ho Chi Minh City, an average user can see 20–50 food options in a single app launch, within a radius of 2–3km. This means your restaurant is not only competing with neighbors, but also with "online kitchens" several kilometers away. Some important insights to consider:

– The "fast food - under 50k" group: sandwiches, bento boxes, instant pho, snacks.

– The "sit for a long time - experience" group: coffee, milk tea, desserts

– The "convenient - no travel required" group: GrabFood, ShopeeFood

If you open a beverage shop in an area where customers tend to order online more often (you can observe the number of delivery drivers waiting and the frequency of deliveries), then you're likely to lose from the start, even if there are no similar shops nearby. This is why many locations with "no direct competitors" still struggle – because they're losing at the second stage.

Layer 3 is the hidden competition – spatial competition. This is an extremely important layer when choosing a location, but few people pay attention to it. A prime location on a main street isn't just for F&B businesses. According to Vietnamese retail market data, industries that can afford high rental prices are typically: banks, convenience stores, bubble tea shops, pharmaceuticals, and fast fashion. For example, WinMart+, Bach Hoa Xanh, and Circle K currently have thousands of stores (WinMart+ has over 4,500, BHX over 2,700). These chains can accept higher rental prices than smaller F&B businesses because they optimize their operations for chain success. This means that when you rent a space, you're not just competing with restaurants, but with businesses that have stronger financial resources.

From this third stage, two very clear consequences will arise: firstly, rental prices will be pushed up beyond the model's capacity to bear (for example, a space costing 30-50 million VND/month but your expected revenue can only handle 20-25 million VND/month); secondly, you might find a location that is "not meant for you" (for example, a location suitable for quick meals but you open a restaurant with long seating). Many people confuse "beautiful" and "suitable" at this point.

To give you a better understanding, I'll quickly summarize how to read these three layers using a practical checklist:

– Level 1 (direct): How many shops in the same industry are there within a 300-500m radius? What is the average price? How crowded are they during peak hours?

– Layer 2 (indirect): What are customers eating/drinking outside of your industry? How many options are under 50k? Is the online ordering rate high?

– Layer 3 (potential): Which industries are occupying prime locations? Which industries are driving rental prices in this area? Does our model align with that logic?

When conducting market research, I often add a crucial step: I stand there for 15–30 minutes and simply observe. I count the number of people stopping, the number of people passing by, the number of cars that can pull over, and the number of delivery drivers who appear. These numbers, though simple, clearly reflect the flow of money. For example, a location with 200–300 cars in 15 minutes but no designated stopping point is almost meaningless for an F&B business. Conversely, a location with only 100–150 cars but with parking and turning space could be more effective.

My approach isn't about "helping you choose a location," but about helping you see the game correctly. Because once you see it wrong, all subsequent analysis will be wrong as well. Instead of asking "how many competitors are there?", change the question to: "how many options do customers have here, and am I the best option?" When you answer this question with data (not just feelings), the decision will be much clearer.

To conclude with a very important point: choosing the wrong location isn't due to bad luck, but to a lack of perspective. When you only look at direct competitors, you're overlooking a large part of the market. When you look at all three layers – direct, indirect, and potential – you'll see clearly: a good sales location isn't necessarily a "beautiful" location, but one that fits customer behavior, the cash flow of the area, and your own business model. And that "fit" doesn't come from feeling; it comes from correctly reading the competition from the start.

Minh Phan – Site Plus | Choosing the right location.

Last week, my team went to work on a new property in District 10. The house looks great: one ground floor and one upper floor, in a good location, and the landlord is friendly.

I thought I'd secured a smooth deal on the land, but when I went to the ward office to get permission for minor repairs, I was shocked to find out that the house only had a ground floor according to the documents; the upper floor was built incorrectly and hadn't been completed. Now I can't make any repairs or renovations at all. I was truly shocked, but luckily I hadn't spent any money on construction yet. Even luckier, the homeowner cooperated and helped me redo the land registry extract, the current status report, and supplement the legal documents.

But what if the landlord isn't cooperative? The whole team invests capital, decorates, plans the grand opening – only to run into legal problems and… pack up and leave.

Common misconceptions when signing a rental agreement.

1. A house that is being used normally is legal → False, many houses are built illegally, have not been completed, or are mortgaged to banks – but may still be occupied.

There are still people renting them out.

You might think it's a normal place to live, but in reality, that house... doesn't meet the requirements for business. Opening a shop in a house with "incomplete paperwork" means you won't be able to obtain a license, register your business, and could even face enforcement action from inspectors at any time.

2. Thinking that someone else has rented it before and it's safe → Extremely dangerous.

Many properties change hands multiple times because previous owners discover problems – and then quietly withdraw.

As a newcomer, you don't ask questions, you don't check, and you just blindly jump in. A painful lesson learned is that just because you saw a previous shop selling banh mi (Vietnamese sandwiches) here, you think you can open a bun dau (Vietnamese noodle soup with tofu) shop too. Ask for the reason why the previous owner moved out. Otherwise, you'll be the next one to leave.

3. Having a lease agreement is legally sufficient → Not enough, a lease agreement is only one part; you need more:

• Original property documents (not just photocopies)

• Verify the true owner

• Area planning information

• Building permit/completion certificate (if additional construction is required)

• Appropriate land use purpose

If you open a restaurant and your house is on agricultural land or privately owned residential land, you can easily be raided at any time.

4. The landlord said verbally that they could provide the documents later → Trusting them is a death sentence.

Many people reassure you, "Don't worry, I'll handle the permits when needed," but then when you need them... they disappear without a trace. You invest hundreds of millions of dong, and when you need a business registration certificate – nothing happens. There's no documentation, no promises, and the contract must clearly state the responsibility to complete the paperwork before construction or opening. Without it, you're out of luck.

5. The house is in an alley, tiny, surely it won't get inspected → Wrong.

Being small doesn't exempt you from legal risks; some properties are subject to pending zoning plans, or are located in areas restricted to food and beverage businesses, and the more you try to hide it, the more attention you'll attract.

You don't need to know all the laws. But you do need to know clearly: whether the location where you plan to open your shop complies with the law.

Documents are not just a few A4 sheets of paper – they are the basis for protecting your money, time, and effort, and preventing you from losing money foolishly. They also save you sleepless nights.