Having developed convenience stores for over 12 years, I've come to realize one thing more and more clearly: with the convenience store model, the question isn't "is this location good?", but rather "is this location aligned with the customers' daily routines?". And if you look at how these chains are operating, especially when scrutinizing the map, you'll see a very clear pattern: convenience stores are closely clustered around apartment complexes and office buildings.

This is not a coincidence. This is a strategy.

Let's look at the market picture first. According to Q&Me data I read, the convenience store/mini-supermarket group alone will reach approximately 9,703 stores nationwide by 2026. Within this, mini-supermarket chains are experiencing strong growth, especially WinMart+ with 4,592 stores and Bach Hoa Xanh with 2,759 stores. As for the truly convenient store group, close to the quick-purchase, quick-visit, high-frequency model, Circle K has 500 stores, GS25 has 318, Mini Stop 184, Family Mart 172, and 7-Eleven 148. Circle K and GS25 alone have 818 stores, notably concentrated in the two major cities: Circle K has 223 stores in Ho Chi Minh City and 191 in Hanoi; GS25 has 196 in Ho Chi Minh City and 46 in Hanoi.

This number reveals two very important things.

Firstly, this market is no longer in its experimental phase. It's a game big enough that chains understand very well what they need to stick to in order to survive.

Secondly, the strong concentration in Hanoi and Ho Chi Minh City shows that the convenience store model is heavily dependent on urban density, a fast-paced lifestyle, accessibility via walking or quick visits, and especially the demand for repeat business throughout the day. And where does that demand come from? In apartment buildings and office buildings.

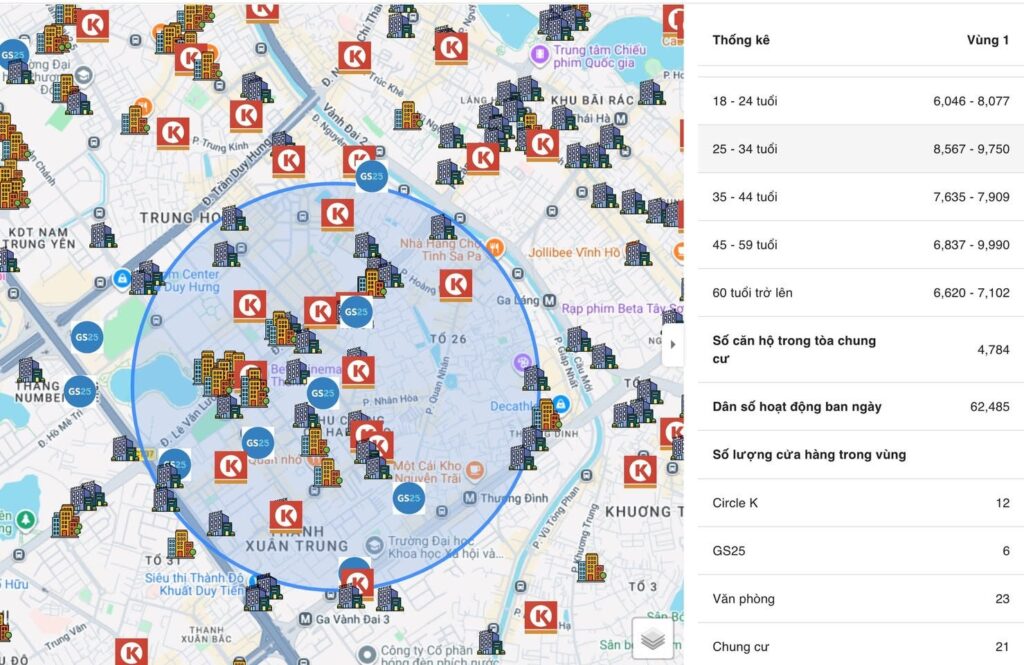

When I looked at the map, the first thing that caught my eye wasn't the number of Circle K or GS25 logos. More importantly, it was how they were strategically placed in areas with high building density, dense residential clusters, and distinct office cores. In the area circled on Mapdy, within the same market zone, there were 12 Circle K stores, 6 GS25 stores, along with 23 office buildings and 21 apartment complexes. Additionally, this area had 4,784 apartment units and 62,485 people with a daytime working population.

This data is very expensive.

Because if you only look at the surface, many people will simply say, "This area is crowded, so there are many businesses." But those in the business won't stop at just "crowded." We need to clearly differentiate: who is crowded, when is it crowded, why is it crowded, and what activities are generating the revenue?.

For convenience stores, the key to survival isn't pure traffic, but rather repeat purchases and convenience on the go. Customers of this model don't always make large, planned purchases like they do at supermarkets. They have very short-term, everyday needs: buying water, coffee, snacks, late-night meals, personal items, paying utility bills, waiting, sheltering from the rain, using the air conditioning, or quickly buying something they forgot to prepare. In other words, a convenience store's revenue comes from many "small transactions," but in return, it requires something extremely large: a continuous, recurring demand around the point of sale.

Apartment buildings create that "repetition" during early mornings, evenings, weekends, and short breaks throughout the day. Office buildings create that "repetition" during rush hour, lunch breaks, afternoons, after-work hours, and even urgent purchases throughout the day. In other words, apartment buildings give convenience stores a resident customer base, while offices give them a daytime customer base. When these two classes overlap, the store essentially generates revenue across multiple time slots, rather than relying on a single peak in sales.

That's why I always say: for convenience stores, a good location isn't just about being "busy," but about having two overlapping rhythms of life. During the day, there are offices generating revenue. In the evening, there are residents generating revenue. And on weekends, there's still the support of the local community. That model is much safer than a location that's only appealing to one group of customers.

Now let's go back to the Mapdy numbers in the circled area. 4,784 apartments represents a very significant population. If we convert that to the number of households, the daily demand for small purchases would be enormous. Not all residents shop at convenience stores, but even a small percentage with a habit of frequenting them would be enough to generate a stable revenue stream. Meanwhile, the 62,485 daytime active residents indicate that this area is not just a place to live, but also a place for work, commuting, and daytime consumption. This is a crucial indicator, as it helps us understand that this area doesn't "sleep" during the day. It has real commercial vitality.

Next, let's look at the competitive structure: in the same area, there are 12 Circle K stores and 6 GS25 stores. Many people might think this indicates saturation. But if you understand the logic of the industry, that's not necessarily true. A large number of stores doesn't automatically mean overcrowding. It usually reflects one thing first: the market is good enough for many chains to operate there. In other words, if an area isn't generating revenue, there wouldn't be so many experienced chains vying for it.

Of course, at some point there will be internal sales competition and pressure. But in the CVS model, the distance between stores is usually much shorter than in other industries, because the nature of the game is about securing the nearest touchpoint. Convenience stores sell "convenience," and when selling convenience, a distance of 200-500 meters can sometimes make a difference. Customers aren't always loyal to a brand based on its products. Often, they are loyal to the store closest to their route, easiest to access, the first to see, and the quickest to enter. Therefore, the chain's strong presence in apartment buildings and offices is not only to attract customers, but also to block competitors, capture customer habits, and secure consumption areas before others enter.

That's why I say the strategy of targeting apartment buildings and offices for convenience stores is a very logical one, very difficult to refute if you look at the true nature of the industry.

Firstly, apartment buildings offer a much higher density of households on a small plot of land compared to sprawling townhouses. An apartment building brings together hundreds, even thousands, of apartments in one location. This means that within a short walking radius, the store has access to a huge customer base. This is exactly what convenience stores need: not a large market, but a compressed market.

Secondly, office buildings generate purposeful traffic, quite different from casual, sightseeing traffic. Office workers consume in a very clear rhythm: morning coffee, snacks, drinks, lunch breaks, personal items, afternoon snacks, and quick purchases after work. They don't need many reasons to buy, just convenience and speed. This type of need is perfectly suited to convenience stores.

Third, by targeting both these layers, the store reduces the risk of dead time slots. A location relying solely on offices is easily susceptible to losses on weekends or evenings. A location relying solely on residents might be weak during business hours. But with both residents and offices, the daily revenue curve is usually thicker, more attractive, and more sustainable.

Fourth, this model also helps the chain optimize logistics and brand recognition. When many locations are clustered in similar urban areas, the chain can easily standardize location selection criteria, expand within the cluster, manage deliveries, and create a sense of "being present everywhere." In the convenience industry, a dense brand presence is a key part of competitive advantage.

But let's be frank: simply being near apartment buildings or offices doesn't guarantee success. This is a common misunderstanding among those outside the industry.

The biggest mistake is viewing apartment buildings as a homogeneous sphere. Not all apartment complexes cater to the same needs. High-end apartments, mid-range apartments, older apartments, areas with strong shophouses, areas with residents who rarely walk to the ground floor, or areas with mini-supermarkets within the complex… each type caters to different consumer behaviors. Some areas have a large population but they shop at large supermarkets weekly, rarely visiting CVS. Other areas have young, single residents who live fast and make small, individual purchases. And in some areas with many apartments, the purchasing power at convenience stores is low due to inconvenient access, difficult parking, or stores being hidden from view on the way home.

The second mistake is viewing office space as merely an added bonus for aesthetics. In reality, having many buildings isn't necessarily a good thing. You need to consider the type of office, its size, occupancy rate, workforce composition, operating hours, whether there's strong competition from food and beverage establishments, and most importantly: the direction of traffic flow from the building. An office across the street that's inconvenient for clients to cross is almost meaningless.

The third mistake is looking at the number of competitors without understanding the context. In some areas, 5 stores are already too crowded. In others, 15 stores still offer opportunities. The issue isn't the absolute number, but rather the overall demand, the distribution structure, and the degree of fragmentation of the customer base. With Mapdy, the key is not just counting competitors, but also understanding which demand segments they're targeting and which areas are truly "breeding ground" for the model.

I want to emphasize another point that store developers must be extremely vigilant about: convenience stores aren't simply about being located in apartment buildings and offices, but about being situated at the intersection of residential areas, workplaces, and transportation routes. Apartment buildings and offices are just two major magnets. To choose the right location, you still need to consider factors like the storefront's visibility, accessibility, parking availability, quick entry points, visibility of the signage, whether the storefront catches pedestrian traffic, and whether evening commuters pass by the storefront. In other words, data helps in choosing the right area. Success, however, depends on selecting the right landing spot within that area.

From a chain strategy perspective, I believe what convenience store chains are doing is more than just "opening stores in densely populated areas." They are building a network that covers the fastest-paced urban areas. They target apartment buildings to retain resident customers, offices to capture daytime consumer traffic, and clusters to increase presence density. And they place stores in locations where customers are likely to visit almost without much thought.

That's why I don't view convenience stores as simply a retail model. They are a model that seizes the power of convenience in urban life.

And if you reread the data you sent, everything fits together perfectly. Q&Me shows that the market is already large enough, competitive enough, and the major chains are still firmly entrenched in the two major cities. Mapdy shows that in a typical market area, there's already a structure that convenience stores love: 4,784 apartments, 62,485 daytime active residents, 23 office buildings, 21 apartment complexes, along with a strong presence of Circle K and GS25. This isn't a random picture. This is a picture of a store expansion strategy based on very clear demand logic.

To sum it up briefly: convenience stores win not because they sell the cheapest products, nor because every location they enter is prime. They win because they understand a fundamental principle of urban retail: to generate repeat sales, they must be located where people repeat their lives. And in large cities, this is most evident in apartment buildings and office buildings. And they are drawn to convenience, as the name suggests.

Image source: Mapdy.vn , Q&Me

Minh Phan – Choosing the right location

Did you find this article helpful?

Sign up to receive new articles every week on store layout and retail development.