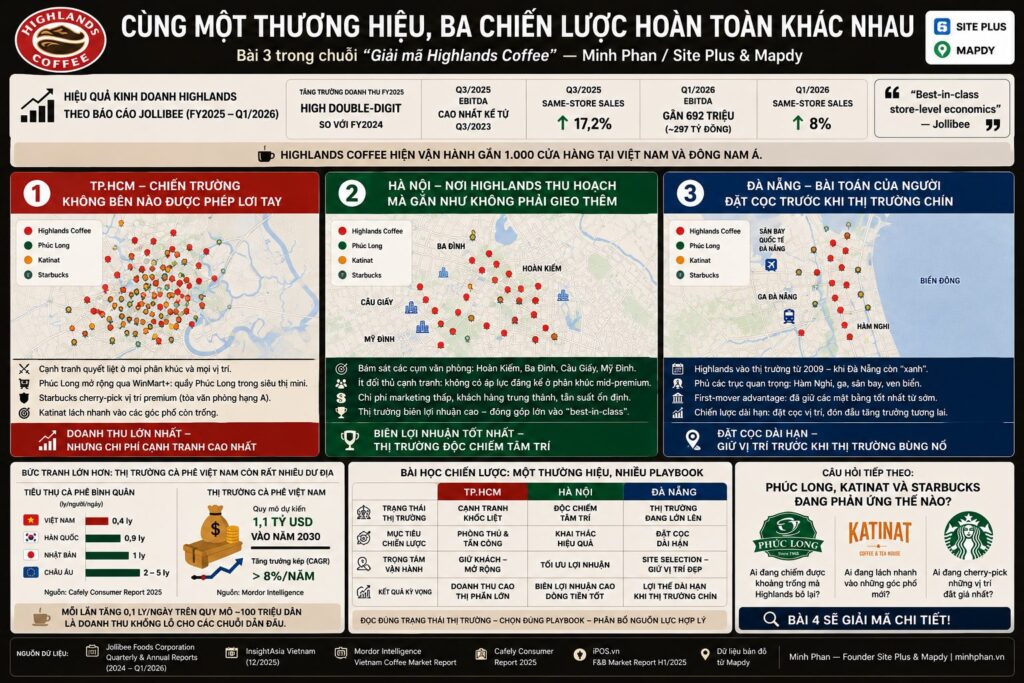

(Part 3 in the series "Reading the Highlands Coffee Map")

At the end of the previous article, I posed a question: which city is bringing in the most money for Highlands Coffee — and not the city many people think it is?

Most people would answer: Ho Chi Minh City. The biggest, most populous, and most dynamic city. But when I carefully read the financial report of Jollibee Foods Corporation — the parent company that holds 60% shares in Highlands — combined with location data on Mapdy, my answer leans towards: Hanoi is giving Highlands the best profit margin, not Ho Chi Minh City.

It's not because Hanoi has more stores. It's because Hanoi is a market where Highlands has virtually no competition — and in business, a market without competitors is a truly profitable market.

To explain why, I need to tell the story of each city and put it alongside the numbers from the report.

Before delving into each market, there are some background figures I'd like to present to give this article a factual basis, rather than just subjective analysis.

Jollibee announced that Highlands Coffee's revenue growth in FY2025 is expected to be double-digit compared to FY2024. In Q3/2025 alone, EBITDA reached PHP 666 million (~$11.3 million) – the highest quarterly figure since Q3/2023, when Jollibee began reporting separately for Highlands. Same-store sales in that quarter increased by 17.21 TP3T – a figure that any chain in the industry would envy. In Q1/2026, EBITDA is projected to reach nearly PHP 692 million (~VND 297 billion), with same-store sales continuing to grow by 81 TP3T. Jollibee used the phrase “best-in-class store-level economics” to describe Highlands – meaning that the business performance at each location is among the best in the group's entire portfolio.

This isn't a random number. It's the result of a point selection and operation system that has been optimized over many years. And to understand why that system works so well, you have to look at the Mapdy map by market.

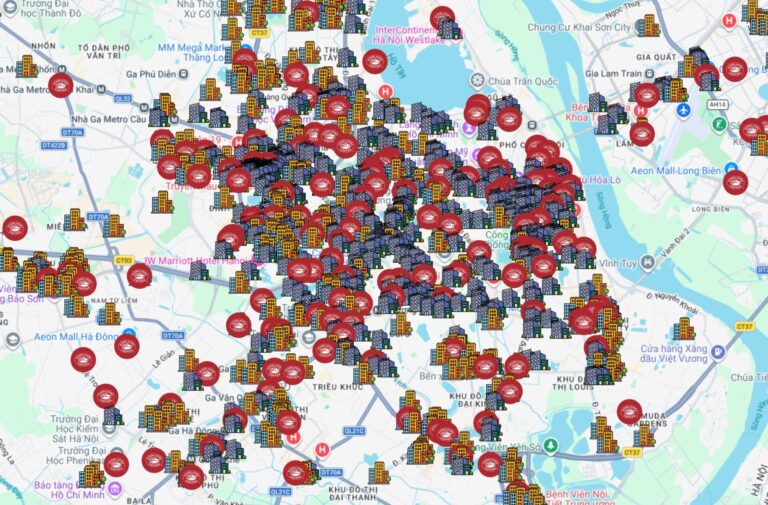

Ho Chi Minh City — A battlefield where neither side is allowed to ease up.

Looking at the Mapdy map of Ho Chi Minh City, what I see is competition taking place on multiple levels simultaneously. Highlands Coffee has a dense presence from the city center to the outskirts. But unlike Hanoi, the red color of Highlands Coffee in Ho Chi Minh City has to share the map with brands strong enough to steal customers at any time.

Data from InsightAsia Vietnam at the end of 2025 reveals a very clear competitive landscape: Phuc Long operates 237 stores, Katinat 114 stores, and Starbucks 140 stores. The majority of the presence of all three brands is concentrated in Ho Chi Minh City. Phuc Long originated in Ho Chi Minh City and understands this market in many ways. Katinat is rapidly encroaching on street corners that the two giants haven't yet captured. Starbucks doesn't compete directly in terms of density but cherry-picks the most valuable locations — especially the ground floors of Grade A office buildings, areas that Highlands also wants to occupy.

A few years ago, Phuc Long expanded its store network through the Winmart+ system, placing Phuc Long counters directly inside mini-supermarkets — a distribution channel that Highlands hasn't yet responded to. When customers become accustomed to buying a cup of Phuc Long coffee while shopping at the supermarket, this habit directly competes with the habit of stopping by Highlands on their way to work, a problem that remains unresolved, and currently only a small number of customers still shop at Winmart+ stores.

This creates a very different operational pressure compared to other markets. In Ho Chi Minh City, Highlands must simultaneously defend and attack — keeping existing locations from being poached by competitors, while continuing to expand to avoid losing new territory. Ho Chi Minh City is the city that generates the most revenue — but also the one that consumes the most competitive costs in the entire system.

Hanoi — Where Highlands are harvesting with almost no need for further planting.

The Mapdy map of Hanoi tells a completely different story.

When Highlands' data is fed into the office sector on Mapdy, the map becomes incredibly clear: Highlands' red dots perfectly align with concentrated office clusters — from Hoan Kiem and Ba Dinh districts to Cau Giay and My Dinh districts. And in Hanoi, there are almost no competitors strong enough to challenge them for those locations.

Phuc Long has a presence, but it's sparse and lacks a clear expansion strategy in the Northern market. Katinat is almost absent—this brand is still consolidating its market in the South. Starbucks appears in some upscale locations but doesn't create widespread competitive pressure. The reality of the Hanoi market shows one thing: when Northern office workers want to drink mid-range chain coffee, their default choice is almost exclusively Highlands.

What does this mean in practical terms? Highlands in Hanoi doesn't need to spend heavily on marketing to retain customers — because there aren't enough comparable alternatives. Habits are formed over years, visit frequency is stable, and customer retention costs are significantly lower than in Ho Chi Minh City. CEO David Thai once shared that Highlands prioritizes resources for product quality first, then marketing — a strategy that can be more effective in a market where the brand already dominates the minds of consumers, like Hanoi.

In retail finance, this is characteristic of high-margin markets: absolute revenue may be lower than in Ho Chi Minh City, but the retention rate after operating and marketing expenses is significantly higher. The phrase "best-in-class unit economics" that Jollibee used to describe Highlands — I believe Hanoi is the market that contributes the most to that "best-in-class" status.

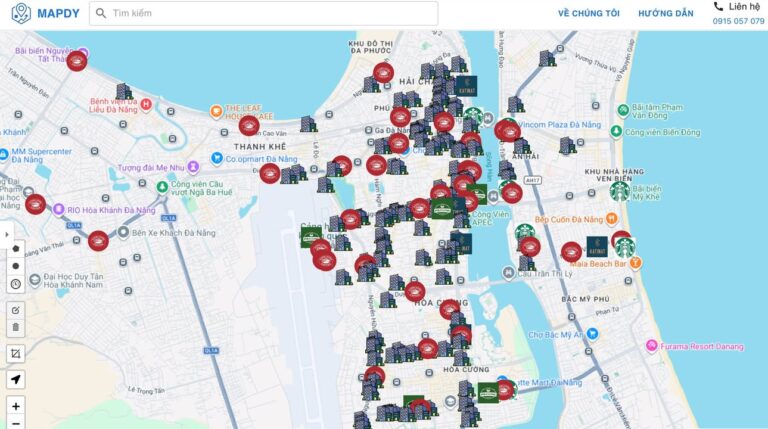

Da Nang — The dilemma of those who place deposits before the market matures.

Da Nang is smaller than the other two cities in terms of size. But the Mapdy map here tells a story about strategy that, in my opinion, is the most interesting of the three cities.

Highlands Coffee has a strong presence along the most important routes: along Ham Nghi Street — the city's densest concentration of offices and commercial hotels, the area around Da Nang train station, near the international airport, and the eastern coastal road. Katinat is just starting to appear in a few locations. Phuc Long is scattered. Starbucks is present but focuses on the high-end tourist segment — a completely different customer base.

It's important to reiterate: Highlands entered Da Nang in 2009, before the city experienced the wave of 5-star beachfront resorts and the real estate boom of 2015-2019. They came when the market was still green and land costs were low. As Da Nang grew, the best locations had long since been acquired.

This is the pioneering principle in choosing a location that I always tell my clients: opening early isn't because the market is ripe, but because when it's ripe, there won't be any good spots left. If Katinat or any other brand wants to enter Da Nang now to compete directly with Highlands on the same street, the cost of space will be much higher than in 2009 — both in terms of rent and the scarcity of remaining prime locations.

The bigger picture: the market still has plenty of room for growth.

One figure I found noteworthy in the Cafely 2025 report: Vietnamese people currently drink an average of about 0.4 cups of coffee per day. This compares to Japan's 1 cup, South Korea's 0.9 cups, and European countries' 2 to 5 cups. Meanwhile, according to Mordor Intelligence, the Vietnamese coffee market could reach $1.1 billion by 2030, with a compound annual growth rate of over 8%.

This means that all three cities—Ho Chi Minh City, Hanoi, and Da Nang—are not yet close to reaching true saturation point. Vietnamese people are drinking more and more coffee, and every increase of 0.1 cup/day across a population of nearly 100 million represents a huge amount of revenue flowing into the chains that are dominating consumer habits.

This is why Highlands' strategy—spreading early, establishing habits first—is not just a story of today. It's how they're placing their bets on a market that will be much bigger in the next few years.

When comparing the three cities, what I noticed most was that Highlands doesn't use a single formula. In Ho Chi Minh City, they operate on a defensive and offensive basis — investing heavily to maintain their territory and continuously improving to avoid losing customers to competitors. In Hanoi, they are in exploitation mode — focusing on efficient operations to maximize profits from a market with virtually no comparable competitors. In Da Nang, they are investing for the long term — accepting some less-than-optimal aspects to ensure no one can snatch up prime locations as the market grows.

Many F&B brands fail when expanding because they find a template, replicate it everywhere, and then wonder why the same model fails in one market but succeeds in another. Three cities, three different business environments, three different resource allocations — but all stem from the same mindset: understand the market conditions first, then decide what to play.

All I've just analyzed is about Highlands in itself. The really more interesting question is: How are Phuc Long, Katinat, and Starbucks responding? Who is filling the gaps on the map left by Highlands — and who is quietly building an advantage that few people realize? Part 4 will answer that question.

P.S.: This is my personal perspective based on data and real-world experience. It's neither entirely right nor entirely wrong, so please read it as a reference. I'd be happy if you could share your opinions so we can all learn together.

Minh Phan — Choosing the right location

Did you find this article helpful?

Sign up to receive new articles every week on store layout and retail development.